Chart of the Day: Here's proof that Singapore O&M stocks are still too expensive

They might suffer the fate of Korean yards.

Singapore’s largest rig builders have lost much of their value in the past year, in line with the sharp drop in oil prices. However, analysts at Macquarie warn that stock valuations could sink further if rig orders vanish and more customers defer delivery.

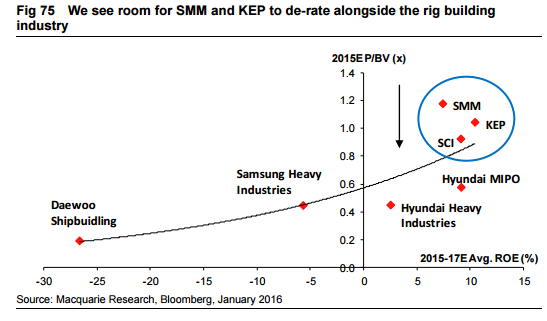

This chart from Macquarie shows that Sembcorp Marine and Keppel Corporation are still valued higher than their Korean peers, such as Daewoo, Samsung Heavy Industries, and Hyundai Heavy Industries.

“Though valuations have fallen to GFC lows of 1-1.3x P/BV, we see more downside and expect multiples to de-rate further to reflect the worse-than-GFC conditions, in our view.

When stacked up against closest rig building peers Daewoo, Samsung and Hyundai, valuations for KEP and SMM are still expensive, further driving our case that SG yards have yet to de-rate sufficiently alongside the rig building industry,” said Macquarie.

The report warned that equity value could go below book like Korean yards if orders get cancelled, particularly orders from corruption-riddled Petrobras.

“Korean yards have long traded below book value as they have generated single-digit returns amidst <100% yard utilization. For SG yards, if 2011-14 orders start getting cancelled, we believe their valuations could go the same way,” Macquarie said.

Advertise

Advertise