Singapore's big developers vulnerable to shocks amidst rising debt

In 2007, Singapore developers’ debt was only around 6% of the GDP, whilst in 2016, it has more than doubled to almost 14%.

Despite a tightening of macroprudential measures and a slowdown in credit growth, the rise of property prices and debt accompanied with weak profits in Asia can cause some Singapore developers to be concerned, the Bank of International Settlements (BIS) said, “The firms are thus vulnerable to shocks, such as increases in interest rates, falling property prices or local currency depreciations.”

BIS analyst Michael Chui said developers’ debt in Singapore in the late 2000s to 2016 has risen significantly, similar to China, Indonesia, Malaysia, and Thailand. “Only Hong Kong bucked the trend as developer debt peaked as a share of GDP in 2014,” he added.

In 2007, Singapore developers’ debt was only around 6% of the GDP, whilst in 2016, it has more than doubled to almost 14%. Moreover, bank debt of resident property firms is 29% of GDP, compared with just under 15% in BIS’ sample.

BIS noted that in most economies, the increase in property developers’ lending coincided with an increase in their leverage. Debt-to-assets ratios of the median firm increased between 2010 and 2016 in all economies, including Singapore.

“That said, debt ratios are still relatively low. Debt accounts for less than one-third of the total assets of the median developer in all the economies studied except China, Singapore and Thailand, where the ratios are just below 40%,” Chui added.

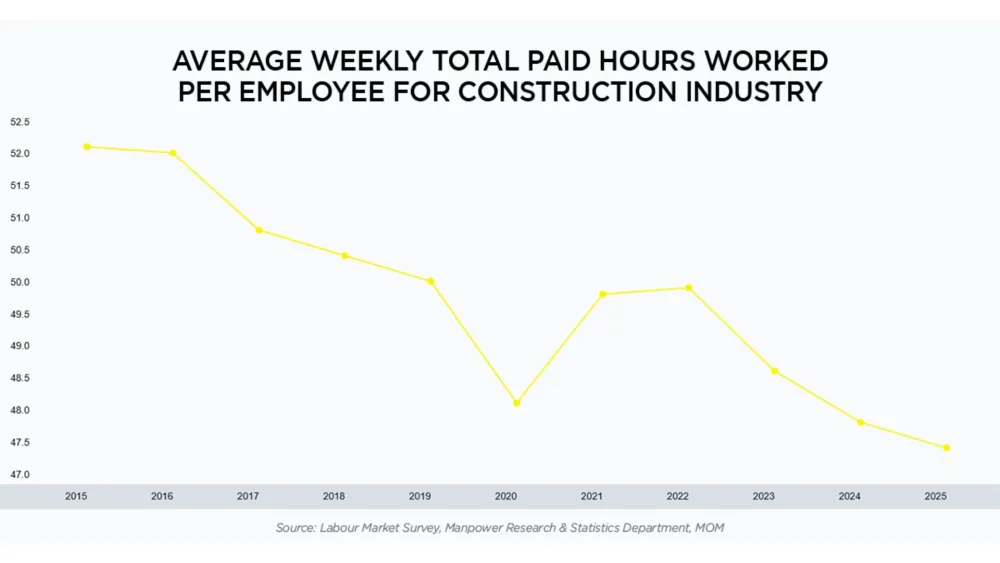

Also read: Construction sector to weigh down 2018 GDP growth

Moreover, Chui noted that the relatively low leverage helps explain why developers have so far not had major difficulties in servicing their debt, despite low asset returns. “Interest coverage ratios – defined as earnings before interest, taxes, depreciation and amortisation (EBITDA) divided by interest expense – have been gradually decreasing in all economies except Hong Kong and Malaysia, but tended to remain well above critical levels in 2016.”

In 2010, Singapore developers’ debt as a share of total assets reached 33.8%, and slightly rose to 35.6% in 2016. Meanwhile, interest coverage ratio dropped from 10.5% in 2010 to 3.7% in 2016. The percentage of inventories in Singapore developers’ assets also fell 21.8% to 18%.

“So far indebtedness has tended to be low for most firms, but weak profitability and declining interest coverage ratios give cause for concern. The firms are thus vulnerable to shocks, such as increases in interest rates, falling property prices or local currency depreciations,” Chui said.

BIS observed that dollar-denominated developer debt appears to be rising overall, although the trend varies across countries. “Whilst in Malaysia, Singapore and Thailand companies have mostly issued bonds in domestic currencies, those in China, Hong Kong and Indonesia have issued considerable amounts of US dollar-denominated bond,” the bank said.

However, Singapore is still significantly affected by the rise of dollar-denominated debt, Chui noted. “Some of the US dollar borrowing has funded activities in foreign currencies – for example, the strong expansion of Chinese developers outside China. In Singapore, Chinese companies have bid aggressively in residential land auctions. In Malaysia, they accounted for almost 30% of the funding of Iskandar Malaysia, a large real estate project in the region neighbouring Singapore,” he added.

The project in Malaysia was intended to establish around 336,000 new private residential units – more than the entire existing stock of private homes in Singapore. “While these projects could bring in foreign currency revenues, these may not necessarily be in the same currencies as the debt that finances them,” Chui said.

Looking back at history, large Asian property developers substantially increased their indebtedness during the property booms that followed the Great Financial Crisis (GFC). Chui explained, “The near-term financial stability risks associated with this debt appear to be limited. Whilst debt levels of property developers are quite high in some economies, approaching 30% of GDP at end-2016 in Hong Kong, 15% in Singapore and 5% in China, leverage looks modest and interest coverage ratios are above critical levels.”

Chui noted that from a longer-term perspective, the sector’s deteriorating fundamentals give reason for concern. “Profitability has declined since the boom years at the beginning of the decade, and many firms’ returns on assets are below their costs of debt. This also means that leverage has been rising and interest coverage ratios falling,” he said.

Advertise

Advertise