Sinarmas Land defends IFA valuation in Lyon Investment privitisation offer

SGXRegCo is questioning how the IFA derived the 20% to 22% holding discount figure.

Sinarmas Land defended the valuation methods of W Capital Markets Pte. Ltd, the independent financial advisor (IFA) appointed to advise the company’s Independent Directors in the privatisation deal with Lyon Investment in response to queries raised by the Singapore Exchange Regulation (SGXRegCo)

The government regulator raised two queries in response to the IFA Letter and its 6 May 2025 update on the offer.

SGXRegCo questioned how the IFA derived the 20% to 22% holding company discount and asked for both the supporting details and comparable examples from past SGX-listed offers.

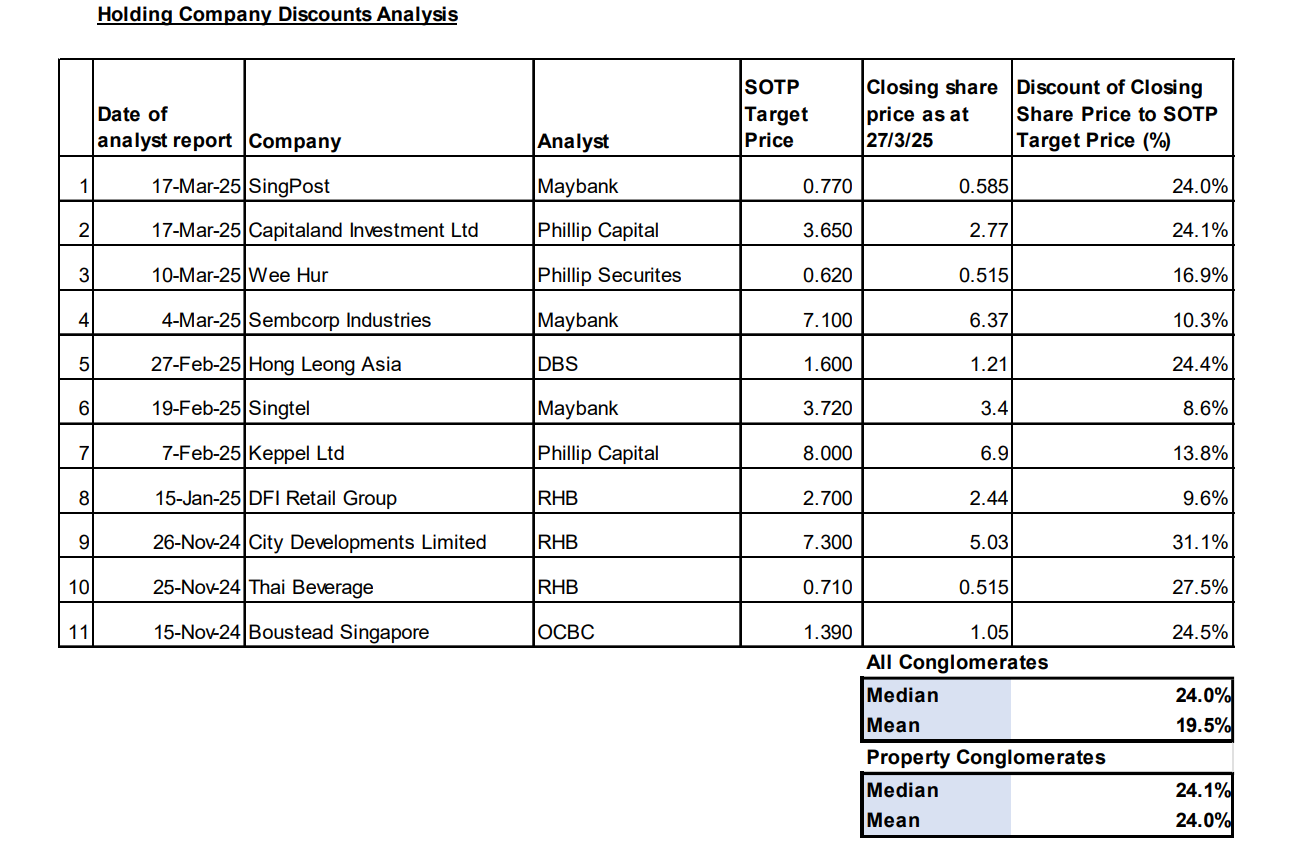

In a bourse filing, Sinarmas Land said the IFA based the 20% to 22% discount on the mean and median discounts, 19.5% and 24%, respectively, of 11 SGX-listed mid to large-cap conglomerates, including property firms, as of 27 March 2025, citing companies such as CapitaLand Investment, City Developments, and Wee Hur Holdings.

“In addition, it is noted from the above that the Property Conglomerates has an implied holding company discount of approximately 24%. In view of the above analysis, W Capital Markets has applied a holding company discount range of 20% to 22%, which it deems to be a reasonable range to adopt,” Sinarmas Land said.

Advertise

Advertise