LBC rates hike to have minimal impact on overall land market

Short-term investment activity is expected to remain reserved.

Revisions in the land betterment charge (LBC) rates for 1 March to 31 August 2025 are expected to not have an adverse impact on the overall market activity, according to JLL.

The Singapore Land Authority recently announced adjustments to the LBC rates for six use groups, namely commercial (A), residential landed (B1), residential non-landed (B2), hotel/hospital (C), industrial (D), and place of worship/civic and community institution (E).

Chua Yang Liang, head of research and consultancy for Southeast Asia at JLL, said the changes “articulated the underlying mood in the Singapore land market, and the Chief Valuer would have used transactional evidence to support the market assessment.

“Strong upward pressure on the landed housing market could have motivated the Chief Valuer to increase LBC rates across all 118 sectors. In contrast, the lingering upward pressure on values, albeit weaker, is reflected in the marginal upward revision to LBC rates for the commercial sectors, despite no evidential transactions of the underlying land values,” he added.

In Group A, LBC rates increased by an average of 0.6%, with the largest increase of 6.3% from Sector 42 (Orchard Road/ Orchard Turn/ Scotts/ Claymore), within which a 50% stake in ION Orchard transacted for $1.849b in September 2024, said Tricia Song, head of research for Singapore and Southeast Asia at CBRE.

Leonard Tay, head of research at Knight Frank Singapore, sad this was likely due to increases in the prices of some of the strata commercial properties in City Hall/Bugis areas as well as in Orchard Road. Sales activity in the Rochor Planning Area also picked up due to the new sales launch of One Sophia in November 2024, he added.

Chua also said that the “most significant gains of over 4-6% are recorded in the Orchard area (Sectors 41-43), assumingly inspired by the equity transaction of Ion Orchard.”

The B1 use group saw an average increase of 3%, whilst B2 rates increased by an average of 0.3%. Specifically in the latter, Song said the largest increase of 4.4% applied to Sector 48 (Yong An Pk/Jln Kuala/River Valley Close) and adjacent sectors 46 (Leonie Hill/St Thomas Walk/Devonshire Road) and 47 (Dublin Road/Lloyd Road/Oxley Gdn/Oxley Walk).

Chua said the increase in B1 exceeded expectations, whilst Tay said this was not expected since there was no increase in the landed price index in the fourth quarter of 2024.

“Surely, it would not be the intention of the authorities to unnecessarily contribute to housing price increases, even if it were to be in a less direct fashion?” Tay said.

For B2, Chua said the increase in this group was expected amidst “overhanging property cooling measures, high cost and interest rate environment, and overarching global economic and geopolitical risks” that continue to affect investors' and developers' appetite for the market.

Tay, meanwhile, said developers were more cautious when submitting bids at government land tenders which has calmed the growth in development land prices in general. The collective sales market has also remained quiet with only a few enbloc projects successful.

For the increased rates in Group C, Tay said there is investor interest from both institutional and private wealth due to the increasing number of tourist arrivals to Singapore back to pre-pandemic levels, backed by ore meetings, incentives, conventions, and exhibitions events alongside entertainment events by international acts.

Song said the largest increase of 8.8% stemmed from Sectors 93 (Jln Seaview/ Peach Gdn/ Amber/ Parkway/ Marine Parade) and 94 (Cassia/ Old Airport/ Haig/ Joo Chiat/ Telok Kurau/ Frankel/ Siglap). This could be due to Katong Plaza which was sold for $180m in October 2024.

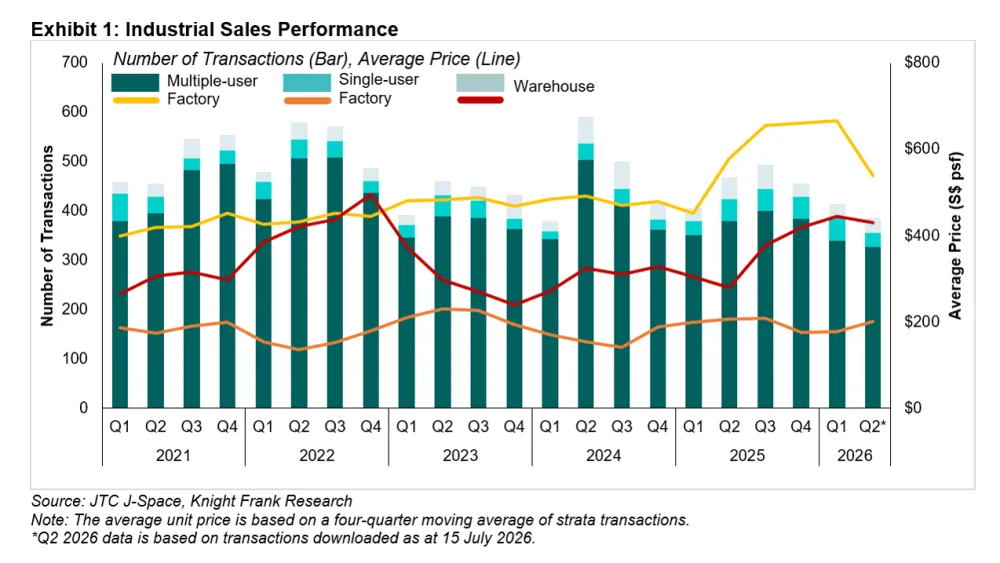

In Industrial D, where rates rose by 0.1%, Chua said uncertain external trade demand ahead has affected developers' confidence.

According to Song, some of the transactions that could have supported the rise include the sale of Admirax (Sector 115) for $155m, 2 Woodlands Industrial Park E1 (Sector 115) for $13.01m, 2 Tuas South Link 1 (Sector 114) for $140.25m, and 21 Jalan Buroh (Sector 114) for $112.80m.

For Group E, Tay said the 5.8% increase is a first since September 2014.

“Again, in a time when costs have increased across the board in all facets of the economy and daily life, was there a need to contribute further tax increases, especially for non-profit usage?” Tay said.

Overall, Chua said investment activity in the short term is expected to remain reserved, “which should limit upward adjustment to the LBC rates, especially in the following review.”

Advertise

Advertise