Singapore construction prices to rise up to 2% in 2025: report

Overall cost growth in the sector is likely to remain slower than in 2024 due to macroeconomic uncertainty.

Tender prices in Singapore’s construction sector are expected to edge upward in 2025, with cost escalation projected between 0% and 2%, following a 1.2% YoY increase in 2024, according to the Building and Construction Authority (BCA) Tender Price Index.

Material costs are showing mixed signals. Steel reinforcement bar prices have fallen to their lowest levels since December 2019. In contrast, copper prices are climbing due to strong global demand and supply constraints, with long-term forecasts suggesting demand could double by 2035.

Logistics costs, whilst currently lower than a year ago, are expected to rise again. The Drewry World Container Index has dropped to US$2,265 per 40-foot container, but reduced shipping capacity and escalating trade tensions could push rates back up.

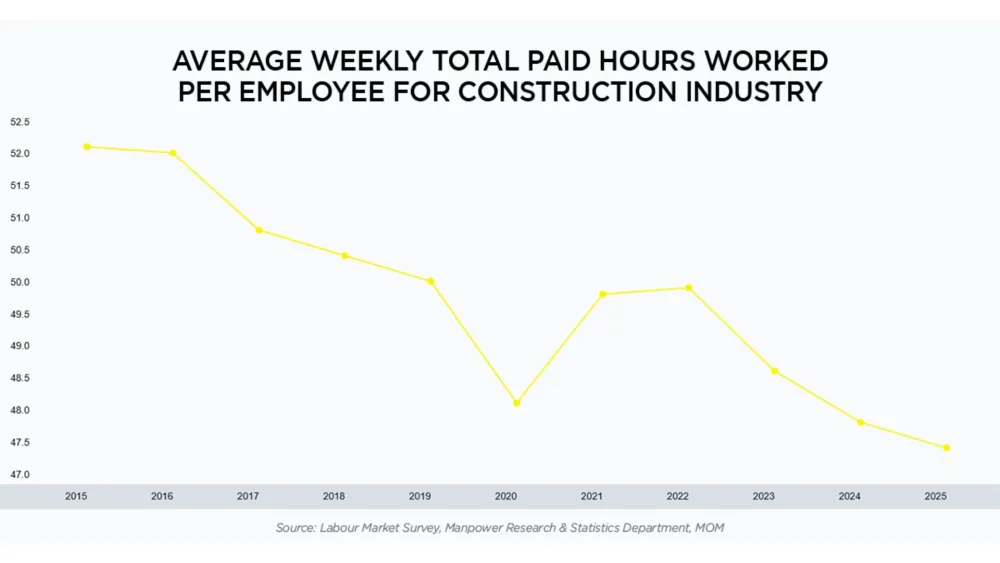

Labour costs are also under pressure. Starting January 2025, the minimum qualifying salary for Employment Pass holders has increased. The minimum salary and levy rates for S Pass holders will go up from September.

Additionally, from June 2025, all construction firms must be registered with BCA’s Contractors Registration System to hire or renew passes for foreign workers, adding another layer of compliance and cost.

The ongoing US-China trade tensions and broader global tariff shifts have introduced volatility that could dampen private sector investment.

Whilst the public sector is expected to sustain demand, private developers may adopt a more cautious stance. This could lead to a more competitive tendering environment, as contractors seek to secure projects amid reduced private capital expenditure.

Mechanical and Electrical construction costs are also projected to continue rising, further contributing to upward pricing pressure.

Despite the steady pipeline of public infrastructure projects, overall cost growth in the sector is likely to remain slower than in 2024 due to macroeconomic uncertainty and subdued sentiment in private development.

Advertise

Advertise