Cautious VCs turn to Series A startups

Early-stage startups in Singapore have raised $50m this year.

Venture capitalists (VC) have become more risk-averse to big-ticket deals and are investing most of their funds in early-stage startups, where the funding market is expected to recover this year after an 18% decline in 2024, analysts said.

“Investors have significant uninvested funds but are focusing their capital towards early-stage companies with strong fundamentals and clear value propositions,” Neha Singh, chairperson and managing director at company tracker Tracxn, told Singapore Business Review.

“Investors are becoming more cautious and prioritising profitability over rapid growth, resulting in a valuation adjustment [for late-stage startups] after a pandemic-driven boom,” she said in a Zoom interview.

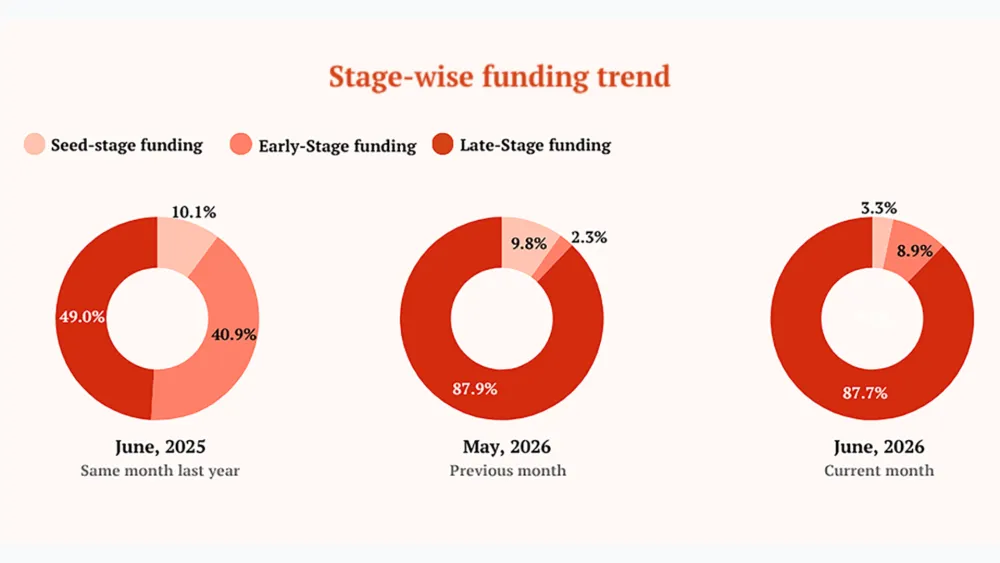

Early-stage tech startups in Singapore have attracted $50m (US$37.5m) in investments as of 23 January, according to data from Tracxn. Early-stage funding comprises Series A and Series B rounds.

Funding for their category fell 18.4% last year to $1.5b (US$1.1b) from a year earlier, though recovery has started, Singh said.

Overall Singapore startup funding fell 56% year on year to $2.8b (US$2.1b).

Bhavik Vashi, managing director for Asia Pacific & Middle East at San Francisco-based tech company Carta, Inc., expects a “tremendous amount of early stage activity” in Singapore this year.

“When you think about early-stage investing, the check size is small, and the valuation, though pretty resilient, is still palatable,” he said in an interview via Zoom. “Fundamentally, you’re making kind of a binary “zero or one” bet when you make an early stage investment.”

“Early-stage investing will still be the most popular and the highest-volume funding stage [this year],” he added.

Early-stage Singapore-based startups that obtained Series A funding last year include BEVM Foundation Ltd. which raised $13.3m (US$10M), and Particle Network Labs, Inc. which took up $20m (US$15m). Polyhedra Network raised $26.7m (US$20m) in Series B funds.

As venture capitalists focused on early-stage startups, late-stage funding in Singapore declined 75% year on year to $944.9m (US$707.7m) in 2024, through fintech, education technology (edtech) and enterprise applications bucked the trend.

Late-stage funding rounds include Series C through Series L, along with unattributed late-stage rounds, according to Tracxn.

Singh said fintech secured $480.3m (US$360m), with insurance platform Bolttech raising $133.4m (US$100m) and cross-border money transfer provider Nium Pte. Ltd. getting $66.7m (US$50m).

Enterprise application startups raised $203.7m (US$152.7m) in late-stage funding last year, led by open-source backend development platform Supabase, Inc. with $110.3m (US$82.6m). Eruditus Learning Solutions Pte. Ltd. was the only edtech startup to secure late-stage funding at $200.1m (US$150m).

Late-stage recovery

Few Singapore-based late-stage companies have experienced valuation growth, Singh said. Valuation for Eruditus rose 7% last year to $4.1b (US$3.1b) from a year earlier, while Bolttech jumped 31% to $2.8b (US$2.1b).

Vashi said low late-stage funding in Singapore and Asia is largely due to the limited involvement of local venture capitalists.

“A lot of companies that reach the growth or late stage often have to go to global funds to raise capital,” he said. “For Series C or D rounds, you typically see US or European investors either leading or participating significantly in those rounds.”

He added that late-stage or growth companies in Hong Kong are in a better position than their Singaporean counterparts, thanks to the China factor. “More investors are willing to provide growth capital in Hong Kong because China is such a big market.”

Singh is optimistic about a potential recovery in late-stage funding in Singapore this year. As of 23 January, late-stage funding had reached $933.9m (US$700m), close to the 2024 total of $944.1m (US$707m).

Singh expects late-stage startups “with strong unit economics and profitability” to continue attracting investor interest and boost their valuations. “Sectors like blockchain and artificial intelligence (AI) are expected to receive increased funding owing to the recent growth trend in funding in these segments.”

Singh and Vashi expect AI startups to attract attention from venture capitalists, particularly those that focus on AI infrastructure.

Singh said edtech startups are also attracting interest from VCs, having raised $204.5m (US$153m) last year.

She identified novel food as an emerging sector, citing Oatside’s $47.1m (US$35.3m) Series B funding round on 24 June 2024. The electric vehicle (EV) sector is also showing promise, she added.

Whilst several sectors have been gaining popularity amongst venture capitalists, fintech startups remain king in Singapore, having raised $1.3b (US$1b) last year. Behind are enterprise applications that raised $796.6m (US$597m) and blockchain technology with $736.9m (US$552m).

Blockchain is also experiencing a resurgence in Hong Kong, where it got the highest seed-stage funding at $161.4m (US$121m), Singh said.

In Singapore, blockchain tech startups were one of the few sectors to experience funding growth in 2024 at 63%, along with edtech, transportation and logistics tech, and food and agriculture tech.

Singh expects 2025 to be a better year for venture capitalist funding in Singapore after a record decline last year.

Vashi also expects a turnaround. “We have probably already hit the bottom,” he said, adding that Singapore’s established frameworks for a strong venture capital ecosystem would support the recovery.

He also expects Singapore being home to many family offices, which often fund venture capital firms that later invest in startups, to quicken the recovery.

Advertise

Advertise